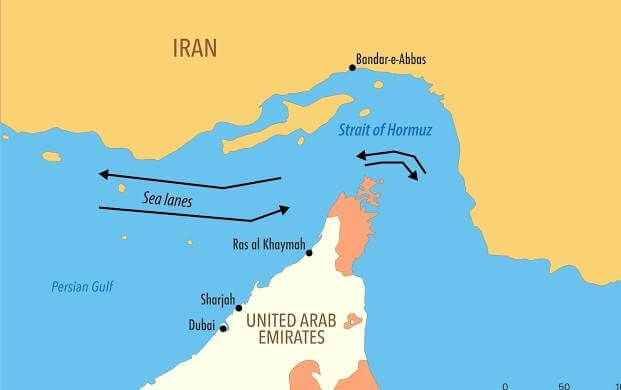

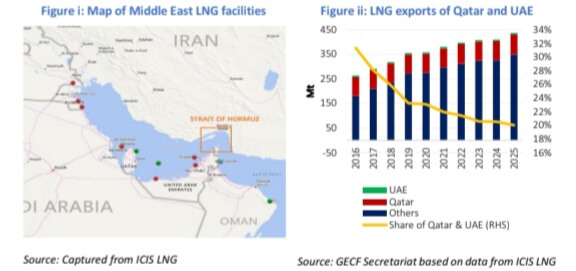

The 2026 Middle East conflict has severely disrupted global LNG trade following the blockade of the Strait of Hormuz, a critical chokepoint through which around 20% of global LNG supply transits (Figure i). As a result, LNG exports from Qatar and the UAE have been halted. Together, the two countries have 83 Mtpa of liquefaction capacity, including 77 Mtpa in Qatar and 6 Mtpa in the UAE.

In 2025, they exported 87 Mt, reflecting utilisation above nameplate capacity and highlighting their role as high-output, flexible suppliers. Although their combined share of global LNG trade declined from 34% in 2015 to 20% in 2025 (Figure ii) due to rapid capacity expansion in the US, Australia, Russia and other exporters, the sudden removal of these large marginal volumes has significantly tightened global balances, with the impact felt most strongly in Asia.

In addition to the short-term operational halt to Qatari and UAE LNG exports due to the shipping blockade, the conflict has affected medium-term export prospects by damaging two of Qatar’s liquefaction trains and sidelining a combined capacity of 13 Mtpa. These trains are expected to require three to five years for full restoration. The conflict has also delayed Qatar’s 48 Mtpa expansion projects, further tightening global LNG supply growth prospects.

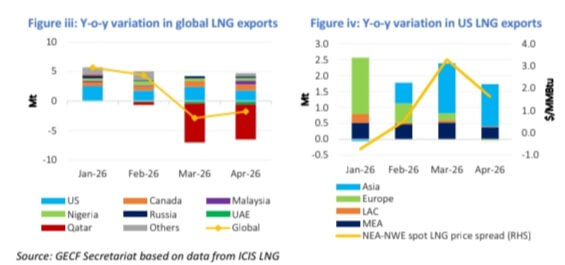

The LNG supply disruptions have placed significant pressure on global LNG trade in March and April 2026, with monthly losses reaching around 7 Mt. Despite this, the global market impact remained relatively contained, with total LNG exports declining by 7% y-o-y in March and 5% in April, as Middle East losses were partly offset by supply growth from other exporters (Figure iii). Nevertheless, the ability to fully replace lost supply remains limited in the short term, with only 24 Mtpa of new liquefaction capacity expected online by the end of 2026. Against this backdrop, the role of US LNG in balancing global supply has strengthened amid the conflict.

In March and April 2026, US LNG exports increased by 2.4 Mt and 1.6 Mt y-o-y, respectively, supported by the ramp-up of production at recently commissioned LNG facilities. While Europe remained the largest destination for US LNG exports, incremental volumes were increasingly redirected to Asia, including 1.6 Mt in March and 1.3 Mt in April 2026 (Figure iv), reflecting tighter regional balances and stronger price signals in Asian spot markets. The destination flexibility of US LNG enables offtakers to redirect cargoes to markets offering the highest netback prices, thereby enhancing short-term supply responsiveness

The outlook for global LNG supply for full-year 2026 will depend largely on the duration of the Strait blockade. Under the optimistic scenario, the blockade is lifted by end-May 2026, allowing global LNG exports to remain broadly stable at 440 Mt in 2026, with higher exports from other suppliers partially offsetting the shortfall. In the pessimistic scenario, disruptions persist through year-end, leading to a decline of 27 Mt, as the loss of Qatari and Emirati volumes exceeds combined gains from ramp-ups and new liquefaction capacity start-ups (Figure v).

The impact of the conflict on global LNG imports has so far been limited. In March 2026, imports declined by only 1.9% y-o-y (0.7 Mt), reflecting the lag between cargo loading and delivery, as many shipments received during the month had been dispatched prior to the conflict. However, by April 2026, the effects became evident, with global LNG imports falling by 12% y-o-y (4.0 Mt). Asia emerged as the region most affected by the crisis, reflecting its heavy reliance on LNG supplies from Qatar and the UAE, with 84% of their combined exports previously destined for Asia.

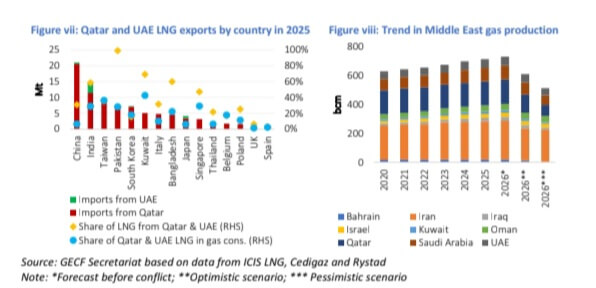

Asia’s LNG imports declined by 1.0 Mt and 3.2 Mt y-o-y in March and April 2026, respectively (Figure vi). China, India, Taiwan, Pakistan and South Korea were among the most exposed markets in terms of lost volumes. Bangladesh, India, Kuwait and Pakistan were the most exposed in terms of LNG import dependence, sourcing over 60% of their LNG imports from Qatar and the UAE (Figure vii). However, the impact on overall gas consumption was lower due to alternative supply sources, including domestic production and pipeline imports

The conflict has triggered a major shock in the LNG shipping market, sending daily LNG carrier charter rates to levels not seen since the peak of the 2022 energy crisis. In early March 2026, daily spot rates for TFDE carriers reached up to $250,000 per day, rising tenfold from early February. The spike was driven by disrupted LNG flows through the Strait, which forced market participants to scramble for vessel capacity. A further factor was the reduction in effective fleet availability, as LNG carriers were increasingly rerouted around the Cape of Good Hope, adding 15–20 days to a typical voyage between the Atlantic Basin and Asia.

In addition, driven by rising crude oil prices, LNG carrier fuel oil costs surged by 73% m-o-m in March 2026. Together, higher charter rates and fuel costs pushed spot LNG shipping costs up by as much as $2.00/MMBtu m-o-m on some routes, adding to delivered LNG prices. Gas production in the Middle East and globally has sharply declined as a result of the conflict. Regional gas output has fallen by over 20 bcm per month, driven by Qatar and the UAE due to suspended LNG production, as well as Iran following physical damage to its gas infrastructure. At the same time, a forced collapse in crude oil output in Saudi Arabia, Kuwait, Iraq and Bahrain has led to a decline in associated gas production.

For full-year 2026, in an optimistic scenario where the Strait of Hormuz reopens by end-May 2026, the Middle East would lose a cumulative 120 bcm of output. In a pessimistic scenario, with the closure extending through year-end, regional losses would reach 220 bcm (Figure viii). In both cases, global gas production decreases, as supply growth in other regions only partially offsets the Middle Eastern shortfall.

Gas demand has also been significantly affected by the global LNG supply shock, driving both immediate demand adjustment and structural fuel switching. Scarcity and price spikes have prompted importers to prioritise energy security over climate objectives. In the power sector, this has led to a short-term shift towards coal- and oil-fired generation, while in industry, high energy costs are resulting in demand moderation.

Governments are introducing emergency allocation frameworks, directing gas supplies to priority sectors such as residential use and fertilizer production. Beyond these immediate disruptions, the prolonged crisis could influence the role of natural gas in the energy landscape. Heightened perceptions of supply vulnerability have reshaped energy security considerations and increased attention to risks for future gas infrastructure investment. In response, many countries are accelerating investment in domestic energy sources, including solar, wind and nuclear power, which could gradually moderate long-term global gas demand growth while supporting broader energy diversification

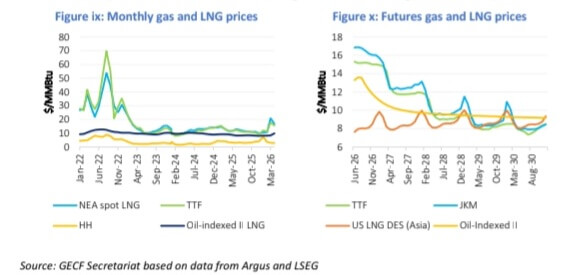

Amid the crisis, a strong price rally has unfolded in Asian and European gas markets. Monthly average NEA LNG and TTF spot prices surged from $11/MMBtu in February to $21/MMBtu for NEA LNG and $18/MMBtu for TTF in March (Figure ix), the highest levels since January 2023, before easing slightly in April and rebounding again in the second half of May 2026.

Prices remain elevated amid uncertainty over the resumption of LNG transit through the Strait and intensifying competition between Asia and Europe for available spot cargoes. Asian buyers were forced to secure higher-priced volumes to offset disrupted long-term LNG deliveries from Qatar and the UAE. In March–April 2026, nearly 100 spot cargo tenders were issued in Asia, up from 89 in the same period in 2025, with India issuing tenders for 44 cargoes, double a year earlier

As of mid-May 2026, JKM and TTF futures point to elevated prices through year-end, averaging $16.5/MMBtu and $15/MMBtu, respectively (Figure x). Prices are expected to soften in 2027 and fall below $10/MMBtu by Q2 2028. JKM is forecast to maintain its premium over TTF in 2026, supporting higher netbacks for flexible LNG cargoes delivered to Asia. In the meantime, the market outlook largely hinges on the assumption that the Strait blockade will be lifted shortly. Unlike the structural supply shock of the 2022 energy crisis, the current disruption is still perceived as temporary, meaning any delay in resolution could quickly intensify market stress and reshape expectations.

If restrictions persist, the perception of a transitory bottleneck would weaken, leading to more sustained price volatility as global supply chains struggle to adjust to prolonged constraints. This vulnerability is further reinforced by concurrent seasonal and regional demand pressures, with Europe needing high gas injections ahead of the winter season and Asia’s expanding gas-fired power demand for cooling amid elevated temperatures associated with El Niño conditions expected in summer. This would intensify competition for LNG cargoes, tightening global supply availability amid rising demand. This crisis has significant consequences for both producers and importers.

Gas producers face operational strain and heightened market volatility, while importing countries bear higher procurement costs and supply constraints, weighing on industrial output, inflation, and global economic growth. A prolonged blockade undermines the reliability of global energy supply chains, increases exposure to sudden shocks, and prompts a reassessment of energy security strategies. It also risks higher emissions, as tighter gas availability and elevated prices force power systems to rely more on coal and oil to maintain electricity supply, thereby weakening international climate commitments and slowing progress on emissions reduction efforts.